Reading List 11/30/24

This week on the reading list: high-rise construction, mild-hybrids, wind power difficulties, offshore drilling, and more. Roughly 2/3rds of the list is paywalled, so become a paid subscriber for full access.

High-rise construction

This graphic shows high-rise construction (buildings 10 or more stories tall) in the US and Canada as of July 2024. It looks like the author manually created this dataset on a sort of city-by-city basis, so (as he acknowledges) it’s probably not 100% accurate. The most interesting thing here is how high Canadian cities rank, both absolutely (Toronto, Vancouver and Montreal are higher than all American cities except for two) and in per-capita terms. Nine of the top 10 cities in high-rises under construction per capita are in Canada, though of course the denominator is doing a lot of work there.

(via statisticurban)

Mild hybrids

Something I hadn’t realized was that many new internal combustion cars are now “mild hybrids," with a small electric motor and battery (and possibly also a regenerative braking system) to assist the gas engine, similar to a full hybrid only smaller. Manufacturers like BMW, Audi, Volvo, and Landrover have most of their gas models as mild hybrids, and 15% of European passenger sales were mild hybrids in 2022. The comparative popularity of mild hybrids in Europe seems to be due to emission regulations.

Via WhichCar.

Wind power struggles

Headwinds for wind power generation (ha!) in the US: most of the best sites are occupied, insurance costs are rising due to extreme weather events, and wind speed is possibly declining due to climate change. The costs of power from wind power purchase agreements are up 13.5% over the last year. Another arrow in the quiver for the “solar will win” crowd.

(via Utility Dive)

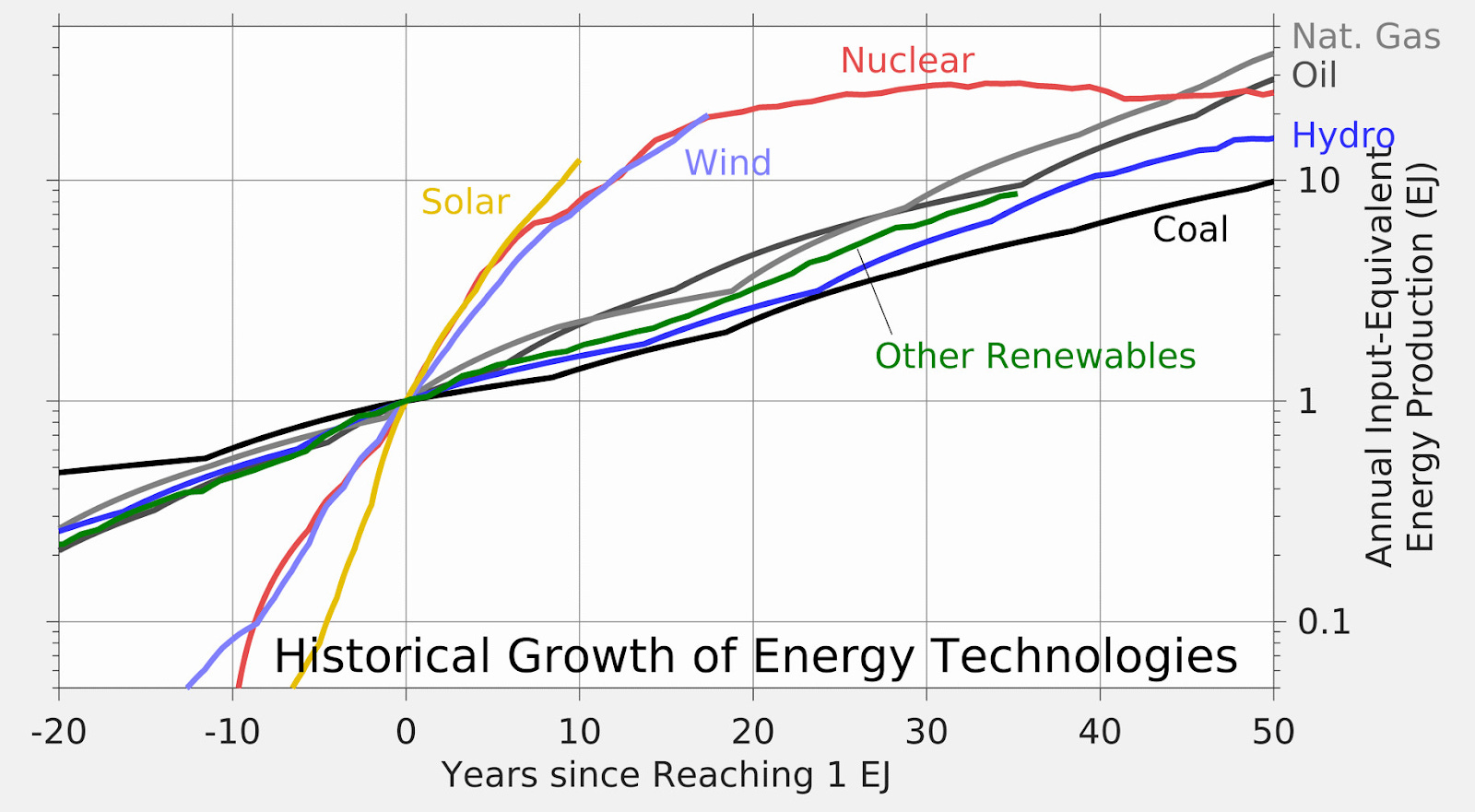

Solar power growth rate

Related, solar power is the fastest growing energy technology in history:

(via Robert Rohde)

Offshore drilling

On the other hand, carbon-emitting energy isn’t going gently into that good night. Deepwater oil drilling is still popular, says the FT:

But plumbing the depths for hydrocarbons is back in vogue. Shale’s once explosive growth has faded and companies are now searching for new sources of oil and gas. Russia’s full-scale invasion of Ukraine caused prices to soar, leaving companies awash with cash at the same time many governments are prioritising energy security over climate targets.

This has encouraged the industry — and its investors — to greenlight new ventures, speed up their exploration of new frontiers in Africa, South America and Asia and drill deeper into the seabed in search of discoveries.

“This comeback looks set to make the 2020s deepwater’s decade,” says Espen Erlingsen, senior partner at consultancy Rystad Energy.

Companies will pour almost $104bn into the space this year, according to estimates from Rystad, up by almost half since 2020 and the highest level since 2016. By 2027, that figure will rise to nearly $140bn.

Partly this is because advancing technology is making deepwater oil cheaper:

The industry’s new offshore model means it can operate much more efficiently than it did before. The average cost of developing deepwater fields has almost halved over the past decade from around $14/boe to $8/boe, according to Rystad.

“In days gone by, we would develop lots of big iron [structures],” says Rich Howe, Shell’s executive vice-president for deepwater. “Today I think our increased activity is much more through small, fast, agile, short-cycle time, smaller assets.”

Technological advances are also allowing the industry to tap previously out of reach barrels, in deeper waters and under ultra-high pressures.

More than 130 miles from Vito, Chevron in August started production at its latest platform, Anchor, which is recovering oil from a reservoir six miles below the water surface.

Related, a huge offshore oil find off the coast of Guyana in 2015 has made the country suddenly incredibly rich, to the point where there’s concern that neighboring Venezuela might invade.