The Rise of Build-to-Rent Housing

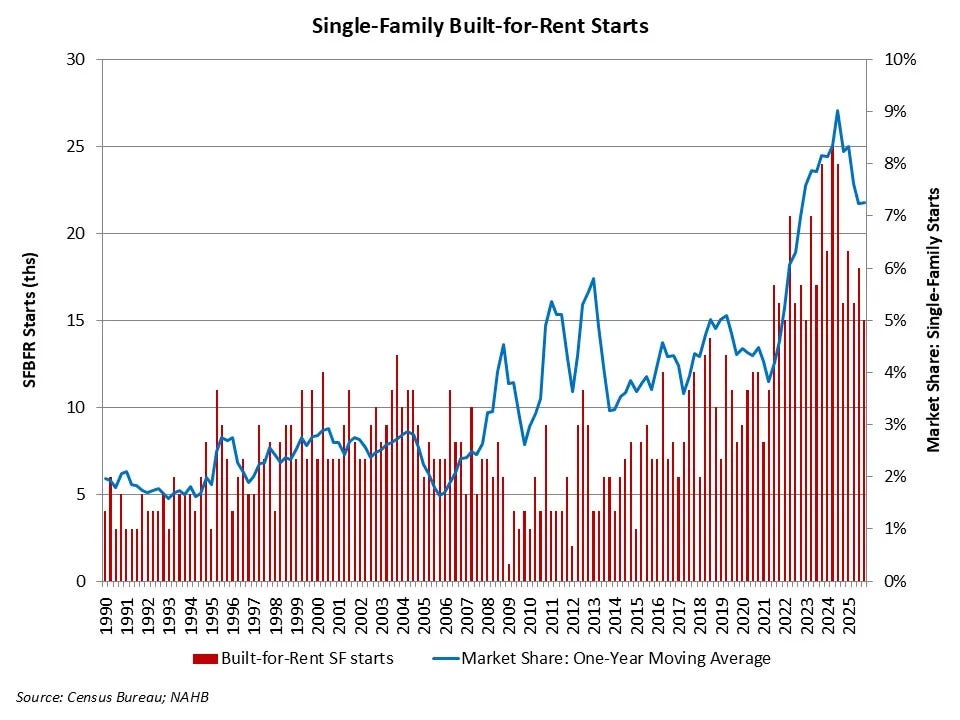

A major shift in the housing market in the last several years is the rapidly increasing popularity of “build-to-rent” homes — single-family homes that are built specifically for the purpose of being rented out. According to the National Association of Homebuilders, build-to-rent homes have risen from less than 2% of new housing starts in the 1990s to more than 7% of housing starts today. In 2025, at least 68,000 new single-family housing starts were built to rent (and due to data limitations, the true number may be much higher, 100,000 homes or more).1

The build-to-rent, or BTR, industry has been in the spotlight recently because of a major federal housing bill, the Senate’s 21st Century ROAD to Housing Act. This bill, which is ostensibly designed to stimulate the building of new homes, includes a provision aimed at preventing large institutional investors from owning single-family homes. This provision, section 901, requires institutional investors (companies that own more than 350 single-family homes) to sell any build-to-rent homes to individual homeowners after seven years. Because BTR involves building a home and then retaining ownership of it to rent out, this provision threatens the fundamental business model of the BTR industry. Since the announcement of this provision, funding for new BTR projects has virtually ground to a halt while investors wait to see whether the bill actually passes. Over 100 pro-housing groups, including Berkeley’s Terner Center, the NAHB, and my colleagues at IFP have come out against this provision specifically, on the grounds that it’s likely to significantly reduce housing supply in the short term.

Because BTR has quickly become such a large fraction of new home construction and is now in the policy spotlight, it’s worth understanding the origins of the industry and why it has become so popular.

Origins of BTR

The modern BTR industry, where developers build entire communities consisting of dozens or hundreds of single-family homes for rent, is a product of the 2008 Global Financial Crisis. Prior to the financial crisis, single-family home rental wasn’t uncommon — in 2005, there were over 8 million detached single-family homes being rented — but the business was mostly the purview of small “mom and pop” operators that owned a relatively small number of scattered rental properties. As late as 2011, no single company owned more than 1,000 rental homes in the US.

But the financial crisis shifted the housing landscape. Huge numbers of people lost their homes to foreclosure: foreclosure rates in 2009 and 2010 were four times rates from 2005, and between 2007 and 2010, there were four million foreclosures. The homeownership rate in the US fell from a high of 69% in 2005 to 63% in 2016. At the same time, to rein in the subprime lending that had precipitated the crisis, banks tightened their lending standards, and average mortgage credit scores rose by more than 50 points. In 2003 buyers with a credit score of less than 620 made up 7% of all mortgages. By 2011 that had fallen to essentially zero.

The raft of foreclosures and the tightening of lending standards had two simultaneous effects on the housing market.

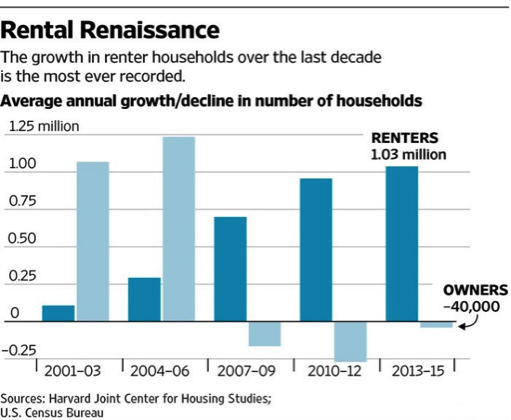

First, they pushed millions of Americans into renting. Between 2010 and 2015 the number of renter households in the US rose by roughly six million, while the number of homeowner households declined by roughly 800,000.

Second, this shift created a huge pool of homes available for purchase at very low prices. Between 2006 and 2010 the value of US homes dropped by 26%, greater than the average decline during the Great Depression. In some markets the declines were even worse: home prices declined by 60% in Las Vegas, and by roughly 50% in Phoenix, Miami, and Tampa.

In response to these market conditions — millions of homes available to buy cheaply, and millions of Americans who couldn’t afford to buy them — various real estate ventures were formed to take advantage of the situation. In 2010, the Arizona-based housing investment company Treehouse Group began to buy distressed mortgages in Phoenix and turn them into rental housing. Within a year the company had purchased 11,000 homes. In 2012 Treehouse was acquired by the investment group Blackstone, which turned Treehouse into the single-family rental company Invitation Homes. Today, Invitation Homes is one of the largest home rental companies in the US, with more than 86,000 rental homes across 12 states.

In 2012, the same year Treehouse was acquired, Wayne Hughes, founder of self-storage company Public Storage, founded American Homes 4 Rent, which similarly began to buy distressed mortgages and turn them into rental properties. Today, American Homes 4 Rent owns 61,000 rental homes across 24 states. 2012 was also when Tricon, a Canadian real estate company formed in 1988, began to buy up distressed mortgages for rental; by 2023, the company owned more than 38,000 of them. While prior to 2011 no single company owned more than 1,000 rental homes, by 2022 the four largest home rental companies owned more than 200,000 of them, largely concentrated in the Sun Belt and Western US.

This large-scale acquisition and transformation of single-family homes into rental properties was encouraged by the federal government, as part of broader efforts to keep the housing market from collapsing completely. In 2012 the Federal Housing Finance Agency launched the REO-to-Rental Initiative pilot program, which “allowed pre-qualified investors to bid on large portfolios of foreclosed properties owned by Fannie Mae.” Roughly 1,800 homes were sold to investors under this program. And in 2017, Fannie Mae backed a billion-dollar loan to Invitation Homes for the purposes of purchasing rental properties.

While most of the new entrants into the home-rental market focused on buying distressed properties, renovating them, and then renting them out, a few companies pursued a strategy of building rental homes directly. NexMetro, founded in Phoenix in 2012, completed its first community of single-family homes built specifically for rent in 2015, and today has built more than 10,000 rental homes across 50+ projects under its “Avilla Homes” brand. BB Living, another Phoenix-based company, also began building rental home communities in 2012, and today operates 18 of them. AHV Communities began construction on its first BTR project in Texas in 2014, and over the next 12 years would build three dozen more.

Building new rental homes had several advantages compared to acquiring existing homes. Being new construction, they typically had much lower maintenance costs than existing homes, and they could be designed by the developer with an eye towards minimizing maintenance and overheads. And because they were clustered together, they were somewhat easier to manage than purchased rental houses that might be spread across a wider area.

As the housing market recovered and the pool of single-family homes available for purchase at favorable prices dwindled, many of the large home rental companies began to experiment with their own BTR strategies. American Homes 4 Rent began work on its first ground-up rental community in 2016; today it owns more than 14,000 BTR homes, with essentially all new home acquisition coming through BTR. Invitation Homes began purchasing BTR homes in 2021 in a partnership with homebuilder Pulte, and as with American Homes 4 Rent essentially all its home acquisition now comes from BTR. Pretium Partners, which owns over 80,000 single-family homes under its “Progress Residential” umbrella, formed a $1 billion BTR venture in 2021. Some companies, such as American Homes 4 Rent, opted to do all their BTR development work in-house, while others preferred to partner with existing homebuilders, buying new houses that developers constructed in bulk.

BTR has attracted the attention of several large homebuilders. Lennar, the second largest homebuilder in the US, began building BTR communities in 2020 under its Quarterra subsidiary (though it has since sold a majority stake in this operation). DR Horton, the largest homebuilder in the US, began building BTR communities in 2019, and last year sold nearly 3,500 BTR homes. Taylor Morrison, the eighth largest homebuilder in the US, launched a BTR brand, “Yardly,” in 2022. BTR can be attractive for homebuilders because it provides them a large stream of steady work and can give them a sort of “escape hatch” if units seem to be selling to homeowners less well than anticipated. (Though apparently some homebuilders refuse to work with BTR companies because they don’t want to be associated with rental housing).

Today, BTR is still a small segment of the overall housing market: CBRE estimates that there are about 350,000 BTR units in the US, which is just 1.5% of the overall single-family home rental market. But it’s a rapidly growing segment of the US housing market — or was, until this recent Senate bill.

What sort of homes are BTR?

“Build-to-Rent” has become synonymous with single-family homes built specifically to be rented out, typically in communities of a few dozen to a few hundred rental homes, but within that category companies offer a broad range of different products. BTR generally gets broken down into several major subcategories (though some use slightly different ones): single-family detached, single-family attached, and horizontal multifamily. These categories exist on something of a spectrum of “very similar to conventional single-family homes” on one end and “very similar to conventional apartment buildings” on the other.

On the single-family home end of the spectrum, you have BTR communities such as Tricon’s Palomino Ranch, built in Houston in 2019. These BTR homes are essentially indistinguishable from single-family homes built for purchase: they’re detached homes with their own garages, driveways, and large fenced backyards. These sorts of homes will be “individually platted”: placed on their own individual plot of land with their own unique address.

On the apartment end of the spectrum, you have what’s known as “horizontal multifamily.” These are BTR developments that are essentially spread out apartment buildings. They are built in a range of sizes typically associated with apartment buildings rather than houses, with 1-, 2-, and 3-bedroom options, and they’re platted together on one large lot. They might have apartment-complex style amenities (gym, clubhouse, etc.), and will typically lack attached garages. They’re attractive to tenants because they don’t have shared walls and they have individual backyards, and they tend to rent for 15–20% more per square foot than a comparable apartment, but in many ways they’re closer to apartment complexes than they are to single-family homes. NexMetro’s “Avilla Homes Deer Valley” community in Phoenix is an example of this sort of BTR development.

Between these ends of the spectrum you have the “single-family attached” category — single-family homes that share one or more walls, such as townhomes or duplexes. BB Living’s Val Vista community of townhouses in Gilbert, Arizona is an example of this sort of project.

Regardless of the layout, a BTR community is at its core a large rental development and is designed by the builder to maximize rents and minimize overhead costs. For conventional homes built for sale, for instance, a builder might simply specify whatever finishes and features a buyer wants. But for a property that the developer is going to hold as a rental, choices are made with an eye towards minimizing maintenance costs by using cheaper, more durable finishes. American Homes 4 Rent, for instance, has stated that due to its designs being optimized for low-maintenance, maintenance costs are just 25% of what they were in their purchased homes.

Home rental companies also have other strategies for trying to minimize their overhead costs. Property taxes, for instance, are often the largest single operational expense for rental home companies. American Homes 4 Rent notes that it’s able to minimize its property tax costs by systematically filing property tax appeals to try and reduce the appraised value of its homes; a 2022 report noted that the company had a dedicated property tax team that filed more than 25,000 appeals annually.

Construction of BTR homes is in large part concentrated in Sun Belt states that have large populations, relatively high growth rates, and space to build new housing developments: Texas, Florida, and Arizona are the top three states for BTR construction, with Georgia and North Carolina rounding out the top five. An estimated 60% of BTR construction takes place in these five states. Within these states, BTR tends to be concentrated in large metro areas: most of Arizona’s BTR takes place in Phoenix, most of Georgia’s BTR is being constructed in Atlanta, and most of Texas’s BTR is being built in Dallas and Houston.

What’s driving BTR demand?

The largest factor driving demand for rental housing, both build-to-rent and buy-to-rent, seems to be housing affordability. Since 2012 home prices in the US have risen faster than inflation and median income. The post-Covid period in particular saw a dramatic increase in home prices, along with a large rise in interest rates that substantially raised the cost of mortgage payments and often made renting more financially appealing than buying. At the same time, Covid drove large increases in the frequency of working from home, which in turn created a demand for larger amounts of living space.

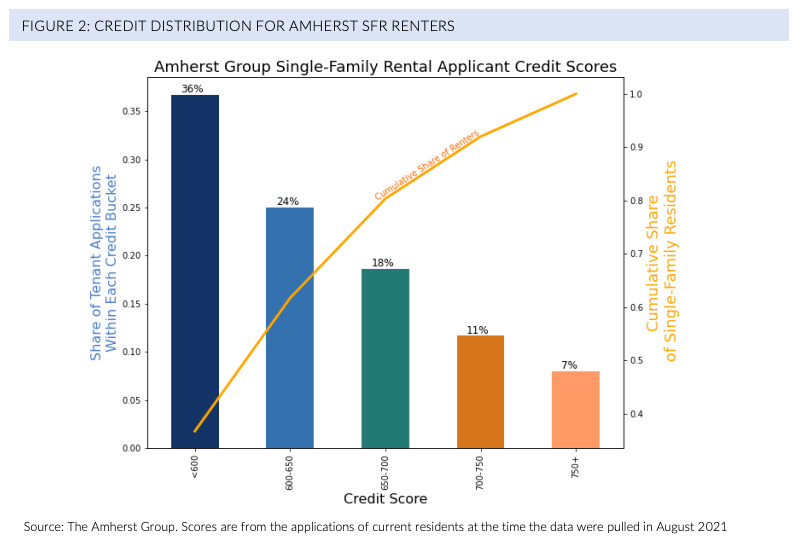

Americans who want more space or more privacy than apartments offer, but can’t afford to purchase a new home, will naturally turn to renting them. Amherst Group, which collectively owns over 50,000 single-family rentals (though not, as far as I can tell, BTR homes), noted in 2021 that 85% of its residents would not qualify for a mortgage due to low credit scores and incomes. NexMetro’s 2024 investor notes the largest factors driving demand for rental housing are rising interest rates and overall home affordability. American Homes 4 Rent’s 2025 annual report states that it has benefitted from “the surge in demand for larger living spaces, and increases in mortgage rates which have made home ownership more expensive.” One BTR developer I spoke to said that many residents simply don’t have the down payment that would be needed to afford a home purchase, and that BTR can give residents a way to access highly desirable school districts that would otherwise be totally unaffordable.

But while affordability issues seem to be the primary driver of BTR’s popularity, there also seems to be some fraction of residents that simply prefer renting over owning, due to a desire for less maintenance or simply because they don’t perceive owning a home as a major life goal. CBRE, NAHB, and NexMetro all mention various demographics of “renters by choice” (such as retirees), an analysis echoed by several BTR developers I talked to. As construction of BTR communities continues, this growth might create a sort of reinforcing cycle: more people move into rental housing, which makes it more accepted, which draws even more people in, and so on.

What’s BTR’s effect on the housing market and home prices?

The effect of large institutional investors (large companies that own thousands of homes) on the housing market has become a major point of controversy. Many, many people have the intuition that companies buying up or otherwise owning large numbers of single-family homes drives up the price of housing, and banning or curtailing this activity has become a popular cause on both the right and the left.

The intuition isn’t crazy. In a normal market, where producers aren’t limited in how much of a product they can make, this sort of purchasing wouldn’t drive up prices because it wouldn’t affect supply in a meaningful way. No one worries about Hertz driving up the cost of cars by buying huge numbers of them to rent out. But housing isn’t a normal market, and in many parts of the US it’s unreasonably difficult to create new housing supply. Ire at large, institutional homeowners would perhaps be more profitably directed at the various supply constraints that make it hard to build new housing in the first place (Invitation Homes notes that it benefits from operating in markets with “high barriers to entry”), but in a world where those supply constraints aren’t going to be removed any time soon, it’s worth considering what effect large rental companies are having on the market.

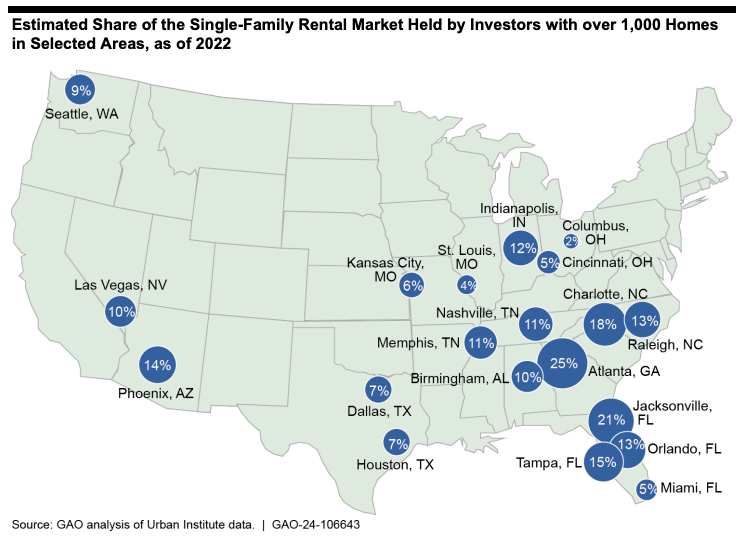

Supporters of rental housing are quick to point out that institutional owners make up a very small fraction of the housing market, less than 1% of single-family homes. However, because institutional ownership is highly concentrated in a few Sun Belt cities, in some housing markets institutional ownership can make up a substantial fraction (up to 25%) of the rental housing market.

There’s some evidence that institutional ownership might drive up home prices. Mills et al. (2015) noted that large scale buy-to-rent investors entering a market tended to “support” (i.e., prevent from falling) house prices in the short term. Lambie-Hanson et al. (2019) estimated that “the increasing presence of institutions in the housing market explains over half of the increase in real house price appreciation rates between 2006 and 2014.” D’Lima and Schultz (2020), Oosthuizen (2023), Coven (2025), Wang and Zhai (2026), Barbieri and Dobbels (2026) and Gorback et al. (2024) all found broadly similar results. However, Hanson (2024) finds that while house prices rise when institutional investors enter a market, this rise can mostly be attributed to improving market conditions, and that prices would have increased whether institutional investors entered the market or not.

The evidence for the effects of institutional ownership on rents, however, is somewhat different. Large owners might use their market power to raise prices (large rental companies will basically admit they raise rents compared to what mom and pop renters would charge), but by buying properties and turning them into rentals investors are also adding supply to the rental housing market, which all else being equal should bring rents down. Lee and Wylie (2024) find that investors raise rents at above average rates when first entering a market. Gurun et al. (2023) found that “institutional landlords leverage their market power to extract greater surplus from renters.” And Hanson (2024) finds that rent growth is due to the market power of the institutional investors. On the other hand, Coven’s (2025) model based on various census and investor property data suggests that added supply from institutional investors can reduce the rent paid by renters, and Wang and Zhai (2026) find that “the majority of renters gain from the expanded rental supply.” Barbieri and Dobbels (2026) find that while the market power of institutional owners raises rents, the increase in supply more than makes up for it, causing rents to fall on net. Economics student Nicholas Decker looks at what he thinks are the strongest papers, and concludes that the net effect of institutional investors entering a market is positive for consumers overall, with the benefits of lowered rents outweighing the increase in house prices.

However, these studies are all for buy-to-rent homeowners: investors buying up homes that already exist. None of them looked at build-to-rent, which we might expect to have substantially different effects: buy-to-rent reallocates existing supply, whereas build-to-rent creates new supply (though it could theoretically also reduce the supply of homes for sale if, in the absence of BTR, for-sale housing projects would be built in the same location).

Unfortunately, the economic research around the effect of BTR specifically is much thinner, and there haven’t been robust studies of the effect of BTR on the housing market specifically.

Conclusion

Overall, I think there are a few points worth making about BTR.

One is that, given that the attractiveness of owning vs. renting can vary depending on the person and the state of the housing market, making a broader array of rental options available for people is a positive thing. I remember years ago when I was trying to find a large (3+ bedroom) place to rent, and how difficult it was to find rentals that size in the area I was looking in. Giving people more ways to purchase housing is good, the same way it’s good for people to have the option to buy or lease a new car.

Second, it’s clear that many folks strongly believe that large-scale corporate ownership of rental housing (which would include BTR communities) is something that can have negative effects on the housing market. But I think it’s more useful to think of the popularity of rental housing as something that’s a product of the housing market: it’s a natural consequence of housing getting increasingly unaffordable thanks to high interest rates and skyrocketing housing prices. Shutting down BTR is a poor way to address that problem; what we need to do is build more housing and develop construction methods that let us construct buildings more cheaply.

The NAHB notes that the 68,000 doesn’t include homes that are built and then sold to another company for rental purposes, which could be an additional 3 to 5% of total housing starts.

There’s one other point worth mentioning on corporate BTR projects. Arizona law requires developers that are going to be selling their properties via mortgages to demonstrate a 100 year supply of water available to the residents. Wholly owned BTR developments don’t fall under this regulation, so they can still build.

Not that this will cause any problems in a desert.

This is an extremely interesting and informative essay on a complex topic. Thanks so much for writing it.

Many years ago my wife and I had a home which we rented out. The renters wanted to buy the house but couldn’t immediately afford the down payment. We crafted an agreement where a percentage of each month’s rent was put aside towards and put toward an eventual down payment at a pre-agreed sales price. There were limitations around how many years the renters had to exercise their buy option and the “escrowed” money was non-refundable.

I don’t understand why BTR homes can’t carry similar options. Real estate has traditionally been — certainly for those who stay in their home — a very solid investment. And while the equity market probably has better long term rewards, people don’t have extra cash to invest in the stock market while they do have money to put a roof over their heads.

Skeptics will say the BTR industry will stop building if they have to insert rent-to-own provisions in their lease agreements. I don’t have nearly enough data to run the numbers but I suspect there’s still a healthy profit to be made as I doubt even 10% of renters would stay say, 7 years, and then exercise their option. And BTR owners would still make a strong return on investment.

There was a time when business meant more than scraping every last nickel off the table. Those days are long gone. And given the increasing importance of BTR, particularly in the south, I don’t have any problem with inserting common-sense rent-to-own provisions that might reduce profits very, very slightly to serve the interests of all Americans.