Reading List 12/07/24

No essay this week; I’m working on a longer piece about the development of polycrystalline diamond compact drill bits, which will be out next week.

This week on the reading list we look at GDP growth by metro, wind and solar bans, battery material consumption, carmaker struggles, Norway and startups, and much more! Around 2/3rds of each reading list is paywalled, so for full access become a paid subscriber.

GDP growth by metro

Joey Politano looks at GDP growth by metro for the last four years:

US GDP by metro & county data finally got released today, and 49 of America's 50-largest metro areas have now recovered from COVID!

Fastest growers have been Austin (+30%), San Jose (23%), Tampa (21%), Jacksonville (21%), & Nashville (21%).

Some interesting trends here: one is the obvious rapid growth of Texas, Florida, North Carolina, and Arizona (these are also the states seeing rapid population growth). It also seems notable that the Bay Area had such a high growth rate. Early during Covid there was a concern about a “techxodus” and predictions that San Francisco was “over.” But despite its numerous problems, it seems to have bounced back, at least somewhat.

Wind and solar bans by county

This map from Brookings shows which US counties have bans or other impediments on wind or solar development:

State and local authorities can implement ordinances and zoning rules that explicitly or effectively ban the construction of new clean energy projects; figure 5 shows a map of counties that USA Today found were doing so. They identified 32 bans against solar and 292 bans against wind, for a total of 324 total bans in 303 counties, 21 counties of which have banned both energy types. In addition, counties have instituted 26 and 17 solar and wind moratoria, respectively.

The most obvious pattern here is the ban on wind in Tennessee and Kentucky, and the statewide impediments in Vermont and Connecticut (these seem to be burdensome setback requirements for wind).

A potentially underappreciated fact about wind and solar is that the energy they capture is very diffuse, so the infrastructure they require will naturally be more extensive than other energy sources. This creates a two-sided pressure against them: it means greater potential opposition to them (since more people will potentially be affected), and it means such opposition will be more disruptive (if you need a lot of land, it's harder to just move an offending operation somewhere else).

Battery materials

Despite the name, there’s not all that much lithium in lithium-ion batteries: lithium makes up the ions that shuttle back and forth, but the lion’s share of the material is the anode and cathode that store them. This is why new cathode chemistries that require less expensive cobalt have been so important to falling battery costs. (For more on lithium-ion battery technology, see my recent essay.)

(via The Limiting Factor)

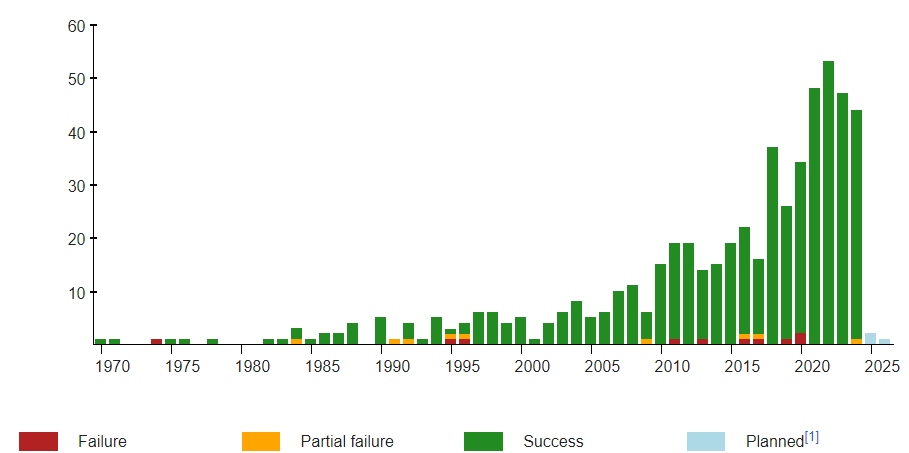

Rocket launches

The reusable rocket aspects of SpaceX get most of the attention, but SpaceX has also managed to steadily increase its launch cadence. The company is close to launching as many rockets in a single year as the Space Shuttle did over the entire life of the program. Via Ars Technica:

So far this year, SpaceX has launched a total of 119 Falcon 9 rockets, for an average of a launch every 2.3 days. The company has already superseded its previous record total for annual Falcon 9 launches, 92, completed last year. If SpaceX achieves its goal of 15 additional Falcon 9 launches this month, it would bring the company's total this year to 134 flights. If you add two Falcon Heavy missions to that, it brings the total to 136 launches.

That is a meaningful number, because over the course of the three decades it flew into orbit, NASA's Space Shuttle flew 135 missions.

The Space Shuttle was a significantly more complex vehicle, and unlike the Falcon 9 rocket, humans flew aboard it during every mission. However, there is some historical significance in the fact that the Falcon rocket may fly as many missions in a single year as the space shuttle did during its lifetime.

Arguably the Space Shuttle isn’t a very good point of comparison, since most Falcon 9 launches are astronaut-less satellite launches, but the Falcon 9 still looks impressive compared to other launch vehicles. Here’s China’s Long March launches by year, from Wikipedia:

Here’s total Russian launches, from r/space:

And here’s US Titan launches, also from Wikipedia:

So not only is SpaceX close to exceeding lifetime shuttle launches in a single year, it’s already exceeded the number of launches the entire Soviet Union achieved at its peak. But it’s also notable how China has steadily been increasing its launch cadence.

Submarine cables

Historically telecom companies like AT&T were the major operator of undersea cables, but increasingly it’s tech companies that are building and operating them. From The Register:

Over the past decade, the amount of international subsea capacity used by the four hyperscalers increased from 10 percent to 71 percent, causing the Australian Strategic Policy Institute (ASPI) to conclude that their influence "hasn't yet been fully recognized or seriously considered."

As the primary drivers of the service that cables provide – a commodity that has surged in demand thanks largely to cloud computing services and AI – it's only smart that the hyperscalers would transition from major customers of cable capacity to owners themselves.

According to one tracking website, Google is a part or sole owner of around 33 subsea cables, Meta about 15, Microsoft 5, and Amazon 4.

In the wake of news about a Chinese ship potentially sabotaging a European undersea cable, it's notable that Meta is also planning a new, $10 billion submarine cable network, in part due to rising geopolitical risk in the Red Sea and South China Sea. From LinkedIn, by way of The Verge:

But the world of submarine cables has major political problems –- in the Red Sea and in the South China Sea which Meta believes are long-term intractable problems, in spite of Meta's large investments in 2Africa. So Meta — after a hiatus of almost 3 years in the subsea space — is planning one hell of a cable that will shock the world.

Dubbed "W" — for its shape, the 40,000 km cable costing $2 billion will be dedicated principally to India. It will start on the east coast of the US and go straight to India with a stop in South Africa (for powering and restoration purposes). And it will also go from India straight to the west coast of the US with a powering and restoration stop in Darwin, Australia — avoiding the Red Sea, the South China Sea and more importantly Egypt, Marseilles, the Straits of Malacca and Singapore — all of which are now major single points of failure.