What Happened to the US Machine Tool Industry?

Machine tools – machines that cut or form metal – are the heart of industrial civilization. Sometimes called “mother machines” (because they’re machines that make other machines), machine tools are required to make almost everything. Nearly every manufactured good is made using machine tools, or by machines which were made using machine tools:

“Thus an automobile is an assembly of metal parts made by machine tools, plastic parts produced by machines made by machine tools, fabric processed on textile machines made by machine tools, rubber processed and molded by equipment made on machine tools, and glass processed by equipment produced by machine tools.” – Anderson Ashburn, Is New Technology Enough?

Being able to manufacture machine tools is often considered an important capability for an industrialized country. Not only does this provide ready access to the latest manufacturing technology, but it ensures production of munitions and other military equipment won’t be bottlenecked by a lack of machine tools. This isn’t a hypothetical concern: American production of artillery shells for Ukraine has been held back by a lack of machine tools. The military has thus historically paid close attention to the machine tool industry and the availability of machinists.

For most of the 20th century, the US was unrivaled in its machine tool technology, and as late as the early 1980s it was the largest machine tool producer in the world.. But almost overnight, the industry collapsed: annual machine tool shipments declined by more than 50% in 2 years, hundreds of machine tool companies went out of business, and the US slipped from the largest producer in the world to the 4th or 5th (depending on the year), roughly where it remains today.

What happened to the US machine tool industry? Why did it fall so far so quickly? Let’s take a look.

The early machine tool industry

Machine tools include metal cutting machines like lathes, milling machines, drill presses, grinding machines, as well as things like wire-bending machines, stamping machines, die-casting presses, and forging machinery.1 Tools like lathes and drills have been in use for thousands of years, but modern machine tools – “power-driven machines with methods of control permitting some degree of precision” – first appeared in Britain at the beginning of the industrial revolution. Watt’s famous steam engine was made possible by the precision boring machine built by John Wilkinson to precisely bore the cylinders for it.

In the US, machine tools were a critical component of the “American System of Manufactures” – interchangeable or near-interchangeable parts produced using a series of specialized machines. This method of manufacturing was first developed for the production of guns (and was thus sometimes known as “armory practice”), and gradually spread to America’s burgeoning industries: sewing machines, locomotives, and especially bicycles. By the turn of the 20th century, thanks to decades of innovation the US was producing the most advanced machine tools in the world.

US technological leadership continued with the rise of the automobile, which created an unprecedented demand for machine tools. As early as 1910, the car industry made up 30% of machine tool sales, which only increased as car sales exploded and car manufacturers adopted mass-production methods (annual car sales went from less than 200,000 in 1910 to 3.7 million in 1925). The car industry required enormous numbers of machine tools (Ford alone eventually had more than 50,000 machine tools in its Rouge assembly plant, roughly as many machine tools as the entire US made in a year), but the demands of car manufacturing pushed machine tool technology forward. Making cars required heavier, more accurate machine tools that could produce more accurate gears, better ball bearings, smoother finishes, and tighter tolerance parts. Machine tool technology was also advanced by the rise of electrification, which enabled machines driven by a series of belts and drive shafts to a central steam engine to be replaced by machines driven by their own electric motor. Between 1910 and 1929, machine tool sales nearly quadrupled, and machines continued to get more and more productive.

Machine tool sales were dragged down by the Depression, but bounced back as production of munitions and military hardware for WWII ramped up (the war also marked the birth of the aerospace industry as the second great consumer of machine tools after the car industry). Annual shipments of machine tools went from 50,000 in 1929, to 5,500 in 1932, to 300,000 by 1942. Over the course of the war, the US produced 800,000 machine tools, and the US emerged from WWII as the largest producer of machine tools in the world.

The post-war machine tool industry

The machine tool industry was shaped by extreme cyclicality: orders for new machine tools might fluctuate 90% year-over-year. This was driven by what’s sometimes known as the “accelerator effect”: a small change in the demand for final goods can cause a large change in the demand for the machines that produce those goods:

Consider a company that manufactures its product on lathes. Assume that it has ten lathes that can just meet production requirements. Assume also that each lathe wears out in ten years and that the company has its investment plans so well organized that one lathe is replaced every year. Now consider what will happen if there is a 10 percent increase in demand for the product. The plant will need eleven lathes to meet production requirements. It will have to buy two lathes: one as a replacement for the worn-out lathe and a second to increase capacity. Thus a 10 percent increase in the demand for the product has produced a 100 percent increase in the demand for lathes. Of course, the accelerator effect is also felt in the other direction. If the demand for the product declines 10 percent, the company will need only nine lathes. In view of the reduced sales volume, it will almost certainly not replace the lathe that has worn out. Thus a 10 percent decline in demand for the product has caused a 100 percent decrease in the demand for lathes. In the real world the relationships are not as neat as in this hypothetical case, but the accelerator effect is a very real factor. – Is New Technology Enough?

This accelerator effect is exacerbated by the fact that machine tools, properly maintained, can last for decades or even longer (the US is still using the 50,000 ton forging press built in 1955 as part of the heavy press program, for instance). An owner of a machine tool can thus put off replacing it almost indefinitely if demand for the product that requires it is uncertain.

The machine tool industry was wracked by such fluctuations in the post-war period. It entered a four-year slump at the end of the war, as wartime demand fell off and the US government sold off huge numbers of surplus machines at rock-bottom prices. Sales then picked back up during the Korean War, fell off again when the armistice was signed, then picked back up, then declined again in the recession of 1958. But the US remained at the technological forefront during this period, and continued to lead the world in machine tool production.

Shifts in the landscape: technology, ownership, competition

In the 1960s, the machine tool industry underwent several major shifts.

The first was the development of numerical control. Prior to the 1950s, there were generally two ways that a machine tool could be controlled. A skilled machinist could manually move the tool and/or the part to be machined to cut it into the proper shape, drill the proper holes, and so on. Alternately, a machine tool could be mechanically automated. Ford, in pursuit of ever-greater efficiencies on the Model T assembly line, built and acquired dozens of different automated and semi-automated machine tools for tasks such as making screws, boring piston heads, and drilling engine blocks.

This sort of automatic machinery had been around since the 19th century, but it was somewhat fixed in the tasks it could perform. The machines couldn’t easily be changed to produce something else without substantially rebuilding the machine (these sorts of difficulties are why Ford had to shut the Rouge factory down for 6 months to retool when changing from the Model T to the Model A, and why auto producers were so interested in robotic welding).2

This changed with the development of numerical control, or NC. With NC, the movements of a machine could be encoded on a paper tape or a punched card. Changing the movements of the machine (and thus what the machine produced) just required feeding the machine a new tape with a different set of instructions.

Numerical control was first developed by MIT’s Servomechanism Lab in conjunction with the Air Force in the 1950s. Early on, the technology had little commercial appeal: it was expensive, complex, unreliable, and designed to solve specific complex fabrication problems in aerospace manufacturing, rather than the simpler machining needs that made up the bulk of machine tool demand. NC technology is sometimes described as “developed from the roof instead of from the foundation”. But that started to change by the early 1960s: machine tool manufacturers began to produce more reliable machines designed for broader commercial appeal (though the technology remained very expensive). In 1958, Kearney and Trecker introduced its Milwaukee-matic, the first of what became an entirely new category of machine tool, the machining center. A machining center contained a tool-changer with dozens of different specialized cutting tools, and could be programmed via numerical control to perform a series of machining operations, automatically changing to different cutting tools as required. This greatly increased efficiency: a typical machine tool was only operational 25-30% of the time, with much of the rest of the time spent setting up the machine and prepping the part to be worked. But Kearney and Trecker boasted that the Milwaukee-matics were operational more than 75% of the time. And because of its ability to flexibly mount different cutting tools quickly and automatically, a machining center could perform tasks which previously required many different machines.

Early NC machines used vacuum tubes, and required large bulky control cabinets as large as the machine tool itself. But NC rode the wave of rapidly improving computer technology: vacuum tubes and paper tapes were replaced by transistor-based minicomputers, and then even smaller microprocessor-based computers, resulting in Computer Numerical Control, or CNC.

NC was adopted slowly: by 1968, just 10% of US metalworking plants had an NC machine, and they made up just 0.5% of total machine tools in the US. But it was clearly becoming a manufacturing mainstay: already by 1968 NC made up 20% of new machine tool sales in the US, and by 1983 had risen to over 40%.

The second major change to the machine tool industry was its ownership. Historically, machine tool companies were small operations run by people (often descendants of the original founders) who had spent their whole life in the machine tool industry and knew it inside and out. Because of the cyclical nature of the industry, machine tool firms tended to be managed conservatively, and they operated with little debt.

But in the 1960s, machine tool companies began to be acquired by the latest fashion in US business, the conglomerate: enormous, diversified companies that seemed to make anything and everything as long as there was profit in it. The machine tool industry was on a sales upswing that showed no signs of slowing, and machine tool firms' high profitability (and low debts) made them attractive acquisitions for the conglomerates. Additionally, the rise of NC technology made the industry seem sexy and futuristic, and many large conglomerates (like Teledyne, Litton Industries, and Bendix) had defense and aerospace divisions, to which machine tools seemed like a natural addition.

The third major shift in the machine tool industry was the rise of foreign producers, especially Japan. Japan’s machine tool industry had been devastated by the war and the immediate aftermath (when many of Japan’s machine tools were shipped to China and the Philippines as war reparations), and by 1955 Japanese tools were just 0.5% of world exports. But Japan was eager to become a major producer of machine tools, and its manufacturers quickly became more capable. Between 1955 and 1960 Japanese machine tool production rose by a factor of 15, and in 1960 American Machinist magazine noted that “Japanese machines for the first time appear to merit recognition and to be competitive with machines of the most advanced industrial nations.” By the end of the 1960s, imports remained a small fraction of the US market (around 10%), but were gaining momentum: between 1964 and 1967, Japanese machine tool exports to the US rose over 1200%.

Fall of the US industry

From the late 1960s through the early 1980s, these trends coalesced in a way that proved disastrous for the US machine tool industry.

Japan had jumped on the NC bandwagon quickly, and began manufacturing NC tools as early as the 1950s. Their progress was aided by dozens of American machine tool firms that were all too willing to license their technology to Japanese producers. (Japanese companies were also not above simply illicitly duplicating American designs). By the end of the 1960s, Japanese machine tool manufacturers were exporting NC tools to the US.

With NC, US machine tool makers had primarily focused on the high end of the market, using advances in computers and other technology to create increasingly precise machines capable of tracing complex paths, and tailoring the machines to the needs of individual customers (as was common in the US machine tool industry). This focus was in part due to the guiding hand of the air force and the aerospace industry, which demanded these types of machines for production of advanced parts. Japanese builders, on the other hand, developed simpler, cheaper NC machines based on standardized designs, aimed at the large, untapped lower end of the market that previously couldn’t justify the cost of an expensive NC machine. And a focus on simpler, standardized designs, along with the traditional Japanese focus on quality, also meant that Japanese tools tended to be more reliable than US tools.

One example of Japanese standardization was controllers, the electronic components used to control the movement of the machine tools. In the US, there were many different suppliers of controllers, and many machine tool builders (like Cincinnati Milacron, Pratt and Whitney, and Warner and Swasey) offered their own, custom-built controllers to try and achieve a competitive advantage. In Japan, on the other hand, the market quickly became dominated by a single producer, FANUC. Not only were Japanese controllers cheaper, but a single standard likely meant that programming the machines and training people to use them was greatly simplified, as there was no re-learning process involved when switching to a different type of control.

Not only were the Japanese building more reliable, less expensive tools than the US builders, but they were delivering them faster. Historically, machine tool companies had dealt with the cyclicality of the industry by acquiring a large backlog of orders, then working it down during the lean times when new orders slowed. When a customer ordered a new machine tool, it might take a year or two (or more) for it to be delivered. One US manufacturer of lathes noted that it built just one size of lathe a month: if you ordered a lathe in February that was only made in January, you’d have no choice but to wait a year for them to build it again. But Japanese builders, with their focus on standardized machine designs, could deliver machine tools in weeks:

“A Pennsylvania company sorely needed a cylindrical grinder, but was told that delivery of a $50,000 American machine would take at least a year. So the company decided to order from a distributor of Japanese tools. Within weeks, it had two Japanese grinders in operation for almost the same price.” – Max Holland, When The Machine Stopped

As Japanese machine tools were advancing, US firms were struggling. Though the conglomerates enjoyed owning machine tool firms in the boom times when profits were high, they quickly became disillusioned during the lean periods when new orders slowed to a trickle. The new owners’ focus on profits meant that they were reluctant to make the long-term investments in R&D or new equipment needed to keep the firms competitive. Between 1968 and 1978, the book value of assets of machine tool companies declined by nearly 50% in real terms.

Conglomerates were often quick to divest their machine tool holdings when the companies began to struggle, resulting in frequent management changes and organizational whiplash as the firms tried to find their footing under new ownership. Storied machine tool manufacturer Warner and Swasey, for instance, was acquired by Bendix in 1980, which then sold it to Allied Corporation in 1983 as part of an effort to fight a hostile takeover from Martin Marietta. Just one year later in 1984, Allied then sold its machine tool group, including Warner and Swasey, to Cross and Trecker, which in turn was bought by Giddings and Lewis in 1991, which then decided to shut down Warner and Swasey the next year. This sort of management shuffling often took place at conglomerates even when ownership didn’t change, as the companies reorganized internally in the face of losses to try and right what they saw as a sinking ship.

Constant pressure to hit quarterly performance targets meant that machine quality often suffered. In some cases, machines would be shipped out the door unfinished so the delivery could be booked, and assembly would be completed by service technicians at the customer’s location. In his history of the American machine tool industry, Albert Albrecht states that “the actions of these larger corporations and conglomerates, under the leadership of financial MBA’s, perhaps more than any other factor, contributed to the restructuring and decline of the US machine tool industry at the end of the 20th century.”

Amidst these struggles, US machine tool builders fell behind technologically. Not only did they lag in the design of low-cost NC machines, but they were well behind Japan in the adoption of microprocessor-based controllers. A 1983 National Research Council Report summarized the situation:

“While many in the industry are convinced that U.S. machine tool technology is presently equal to the most advanced level attained by any overseas competitor, the panel believes that the United States may now have slipped behind the Japanese on control technology and on the software to support such control systems. Additionally, the panel expressed concern that the Japanese are also more advanced in the general development of machining systems that allow round-the-clock operation with minimum human attention.”

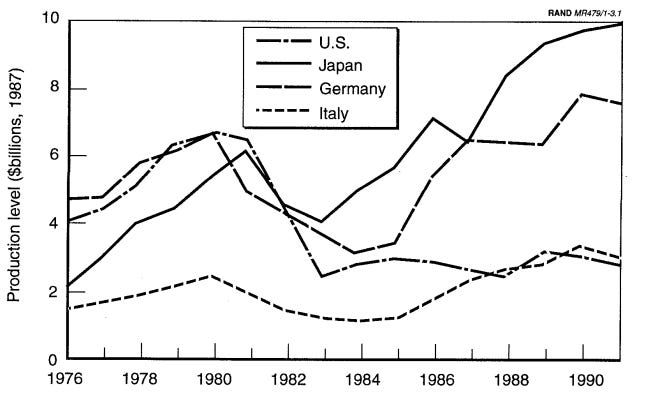

And Japan wasn’t the only country making progress. By 1970, Germany (which had always led the world in machine tool exports) had become the world’s largest machine tool producer (though the US would eclipse it again several years later). And between 1965 and 1980, Italy’s share of world machine tool output tripled. As late as 1973, imports of machine tools were just 10% of the US market, but by the end of the 1970s they had reached 22%.

These trends came to a head in the recession of 1982. Machine tool sales dropped precipitously, falling from $5 billion in 1981 to just $2 billion in 1983. But this time, sales didn’t bounce back. By now, tools from Japan and other countries were as good as or better than US tools, not to mention cheaper and more reliable. A strong dollar made imports even cheaper by comparison, and high interest rates reduced the demand for capital investment. US manufacturers found themselves with uncompetitive products in a highly competitive market. Whereas imports had been just 10% of the US market in 1973, by the late 1990s they were closer to 60%, and by 1986 75% of NC machines were imports. Japan alone made up 50% of the US NC market in the late 1980s.

The US industry collapsed almost overnight. From 1981 to 1983 employment in machine tools declined by a third, and continued to fall (by 1991 it was half its 1981 level). Between 1982 and 1987, half of US machine tool firms closed their doors. The US fell from the largest machine tool builder in the world to third behind Japan and Germany, and continued to decline: by 2002, it had dropped to 5th behind Italy and China, where it remains today.

The industry tried to get some of the same protectionist measures industries like steel had secured. Houdaille, an industrial conglomerate with a large machine tool division, attracted a great deal of attention with a petition to have the investment tax credit denied to Japanese machine tools. But the machine tool industry had much less success with its pleas for protectionism than the steel industry; Houdaille’s petition was denied, and while the industry was eventually able to get some Voluntary Export Restraints (which lasted from the late 80s to the early 90s), it did little to change the overall trends in the industry.

Today, the US competes in a machine tool market that continues to be dominated by Japan, Germany, and now China. It has some bright spots, such as Haas Automation (founded in 1983, in the ashes of the industry’s collapse), but the major producers are all foreign companies. As of 2014, not a single one of the 10 largest machine tool companies in the world was a US company (Haas clocked in at number 13), a fact which as far as I know remains true today. The US is still a major purchaser of machine tools (2nd in the world behind China), but unlike for most of the 20th century, today its factories are full of machines made elsewhere.

There is something of an issue of definition here. Traditionally machine tools were just considered metal cutting machines, and things like die casting or stamping equipment would be categorized separately.

Some flexible machines did exist, such as the Blanchard lathe, which could duplicate the shape of any gunstock placed within it.

> between 1964 and 1967, Japanese machine tool exports to the US rose over 1200%.

Worthwhile to note the reason behind those dates is that the US entered the Vietnam war by shipping a massive amount of full containers across the Pacific ocean which would then make a leg across to Japan to fill their containers for the journey home, massively decreasing the cost of exporting to the US market. A huge chunk of the Japanese economy was put into overdrive via this inadvertent subsidy.

Given how over-used the word "disruption" is (the word in the Clayton Christensen sense), I hesitate to write this, but... this looks like a good case of true disruption. In that the Japanese found it easier to sell simple machines and then upgrade their capabilities, than the Americans found it to bring down the cost of their more advanced machines. I did some consulting work in the 1980s for one of the last independent American MT companies standing, Lamb Technicon, which to its credit spent half its Board meeting time figuring out how to compete... but the other half reassuring itself that the Japanese tools were cheap/uncompetitive/not serious/etc. I think after a series of M&A moves LT is now owned by a German company.