Where Are the Economies of Scale in Homebuilding?

Over the last few months we’ve examined the extent of the construction industry’s productivity problem. We’ve looked at a variety of construction productivity metrics, both for the US and for countries around the world, and found that construction productivity almost always rises much less in construction than it does in industries like manufacturing; often, it doesn’t improve at all. We’ve analyzed trends in construction costs in the US and around the world, and noted that construction almost never gets any cheaper: construction costs almost always rise at or above the level of overall inflation. And we’ve considered the most obvious strategy for solving this problem — moving the construction process into a factory — and we saw that the cost savings from prefabricated construction are frequently much less than hoped, often never materializing at all.

Now that we’ve mapped the contours of the problem, we can begin to explore its deeper nature to understand why, specifically, construction productivity is so resistant to being improved, and why construction costs stubbornly refuse to fall.

We’ll start by looking at one of the most important mechanisms by which production processes can get cheaper: economies of scale. Many processes have lower unit costs as production volumes rise, thanks to a variety of scaling effects: fixed costs can be spread more thinly, equipment gets cheaper on a per-unit basis due to area-volume relationships, improved production methods are developed as a result of learning-by-doing, and so on. However, in construction these effects are modest at best, even in sectors like homebuilding with very large production volumes.

In homebuilding, we’ll see that the limits to these economies of scale are in large part dictated by the nature of the production process. Economies of scale work by eliminating the difference between the costs of the raw inputs to a process and the final costs of production. In a highly efficient, high-volume production process, the costs of the output will gradually approach the costs of the material inputs. But in conventional homebuilding in the US, this difference is already small, giving scale-based strategies relatively little margin to close.

Economies of scale in homebuilding

We’ll examine economies of scale in construction through the lens of housing construction in the US. For many sectors of construction, difficulty in achieving economies of scale could be attributed to the fact that only a small number of buildings of a particular type get built in the US each year. There were, for instance, only 10 skyscrapers taller than 200 meters built in the US in 2025. Semiconductor fabs, urban subways, and airports are similarly built in very small numbers. It’s hard to achieve economies of scale when there’s no scale to be had. Houses, on the other hand, are built in very large numbers. There were over 1.3 million housing starts in the US last year, including 942,000 single-family homes. This isn’t large compared to other types of manufactured goods — the US consumed over 7 billion cans of vegetables in 2025, for instance — but it’s certainly large enough for economies of scale to appear.

However, evidence suggests that homebuilding in the US exhibits relatively modest economies of scale. For one, the level of concentration in the homebuilding industry is relatively small: housing construction in the US is done by a large number of comparatively small firms. A 2022 study by Harvard’s Joint Center for Housing Studies (JCHS) found that the US had over 65,000 firms engaged in homebuilding, and that even the 100 largest firms combined were responsible for less than 50% of the homebuilding market. In homebuilding, the four largest firms held around 18% of the market, compared to 90% in aircraft manufacturing, 86% in wireless telephone service, and 58% in automobile manufacturing. Concentration in the homebuilding industry has been rising over time (primarily due to the growth of the two largest builders, Lennar and D.R. Horton), but it’s still much lower than in many other industries. This level of concentration isn’t what you’d expect to see if economies of scale in homebuilding were substantial.

Another, earlier JCHS study that looked at US homebuilding in the late 1990s and early 2000s found that construction costs were actually higher for the largest US homebuilders than for smaller US homebuilders. It also found that large and small homebuilders had similar gross margins on homebuilding (the difference between the costs to produce a home and what they sold it for). If there were major economies of scale in homebuilding, all else being equal we’d instead expect to see larger firms have lower construction costs and greater gross margins.

More recent data suggest these trends have continued. If we look at the gross margins of public homebuilders, we see virtually no relationship between gross margins and number of homes produced. Lennar, which built over 80,000 homes in 2025, has similar gross margins and average home selling prices to United Homes Group, which sold just 1,192 homes in 2025. LGI Homes and D.R. Horton had nearly identical selling prices and gross margins, but the former sold 4,685 homes in 2025 and the latter sold over 84,000. Looking at different years doesn’t alter the picture much.

This isn’t a smoking gun, as there are other reasons why larger firms might not have higher gross margins than smaller firms. Large firms might be deliberately selling at a lower price to try to capture or maintain market share, as Lennar states it does. But it’s consistent with there being few economies of scale in the homebuilding industry.

In his history of the US homebuilding industry, homebuilder Ned Eichler describes the economies of scale available to homebuilders through the end of the 20th century. While he notes that homebuilders building several hundred homes per year could achieve substantial cost advantages compared to much smaller builders, there appeared to be little advantage in increasing scale beyond that. Writing in the 1980s, Eichler noted that “[n]ot even the largest firm has any of the advantages of dominant companies in other fields… What little technology exists is available to all.”

In the late 1940s and 1950s, as large-scale merchant builders (100 units per year or more) became the dominant suppliers of homes, most of the postwar improvements in production organization and techniques were made. As unit costs began to rise rapidly in the 1960s, because of higher quality, high land and site development costs, and inflation, there was heightened interest in the possibility of another round of increased efficiency from greater scale and technological breakthroughs. Many firms did grow, mostly by geographic expansion. Several broke out of the 100 to 1000 unit range to annual volumes over 5000. By 1980 US Home brought its unit production to 15,000. However, there were no significant changes in technology or even methodology. Nor is there clear evidence that US Home, Ryan, Pulte, or other multicity builders have yet achieved economies of scale.

Today, large homebuilders continue to use the same basic homebuilding methods that much smaller builders do, and builders like Lennar and D.R. Horton effectively subcontract all of their actual homebuilding to local contractors. (Lennar’s 2025 annual report, for instance, notes that “[w]e hire subcontractors for site improvements and virtually all of the work involved in the construction of homes.”) Large homebuilders do note that they’re able to achieve some scale economies by getting volume discounts on material purchases, but evidence suggests that these savings are relatively modest. Group purchasing organizations, such as CBUSA, pool material orders together in order to receive volume discounts from suppliers; CBUSA boasts that it gives independent builders “the purchasing power of a top 10 National Builder.”1 But the savings it offers works out to around $9,500 per house for the builders who use it, or around 6% of the material costs of an average new home.

You sometimes see claims that economies of scale in homebuilding could be achieved with assembly line-style construction, building hundreds or even thousands of homes at once on enormous tracts the way the US did in the 1940s and 50s. But evidence suggests that savings from this style of construction are somewhat modest, and may not materialize at all. Older versions of Craftsman’s National Construction Estimator provide percentage cost deductions for some tasks if they’re done on “tract work,” but these reductions are typically modest (10-20%) and are only available for a small handful of tasks.2 (One exception is carpentry, which does see large labor cost reductions for tract construction in some editions, but this on its own isn’t enough to shift the overall cost of a house substantially.) Likewise, Levitt and Sons famously built thousands of houses in enormous “Levittowns” using a sort of “reverse assembly line”: worker teams would go from house to house, performing a particular set of tasks and then moving on to the next one. But the cost of Levittown houses doesn’t appear to be all that different from those built by other, much smaller homebuilders at the time.

Economies of scale in manufactured homes

We can sharpen our understanding of economies of scale in homebuilding by looking at one particular subset of housing construction: manufactured homes. Manufactured homes, formerly known as mobile homes, are built using largely the same technology as conventional homes, but instead of being built on-site, the homes are produced in a factory, mounted to a steel chassis, and transported to their final location via truck. Roughly 100,000 manufactured homes are produced in the US each year.

Manufactured homes are a useful lens for understanding economies of scale in homebuilding, because they eliminate so many factors that might be expected to restrict them. Economies of scale require repetition — making approximately the same thing over and over again — and such repetition is particularly achievable with manufactured homes:

Conventional homebuilding is subject to different building code requirements in different jurisdictions, depending on what version of the code has been adopted. But manufactured homes are built to one set of national requirements, the federal HUD code.

Conventional homes are constructed on-site, and those sites might have substantial variation between them. But manufactured homes are produced repetitively within controlled factory locations.

Conventional home construction takes place on constantly changing jobsites, with constantly changing construction crews, a constant churn that might disrupt opportunities for learning-by-doing. Manufactured home construction, which takes place within a single location, should be less susceptible to this sort of disruption.

There’s some evidence for greater economies of scale in manufactured home construction compared to conventional homebuilding. Specifically, the manufactured home industry shows substantially higher concentration than the conventional homebuilding industry. The three largest manufactured home producers are Clayton Homes (49,000 units per year), Cavco (about 20,000 units per year), and Champion (roughly 26,000 units per year).3 Together, they make up roughly 90% of the US manufactured home market, similar to the level of concentration we saw in other industries.

However, despite this level of concentration, actual production economies of scale in manufactured home building appear relatively modest. We can see this by looking at the operations of four public manufactured home companies. The first two, Champion and Cavco, produce around 26,000 and 20,000 homes per year, respectively. The third, Legacy Housing, makes around 1,700 manufactured homes a year. And the last, Nobility Homes, makes just a few hundred manufactured homes each year.

Each of these homebuilders is catering to broadly similar segments of the market, since manufactured homes tend to be purchased by lower-income buyers. Their annual reports all note that the typical manufactured home buyer has a low household income, though they disagree on the exact number – Cavco thinks it’s less than $40,000, Champion thinks it’s less than $60,000, and Legacy thinks it’s less than $75,000. As we saw with conventional homebuilders, there doesn’t seem to be much relationship between gross margins on factory homebuilding and production volume. Nobility homes (391 shipments in 2025) and Legacy homes (1703 shipments in 2025) actually have better gross margins on home sales (32% and 28% respectively) than the much larger Champion and Cavco (27% and 23%).

More importantly, all four of these manufacturers use essentially identical production methods. Nobility Homes has one factory in Florida, Legacy has two factories in Texas and one in Georgia, and Champion and Cavco each have several dozen factories spread across different states. These factories are similar: each is typically 100 to 200 thousand square feet, employs 100 to 300 people, and produces several hundred homes a year. In other words, there do not appear to be large economies of scale at the factory level. Even relatively modest production volumes (20,000 units annually) get spread among dozens of different factories. By comparison, a single modern car factory will produce several hundred thousand cars a year.

There are some exceptions to this: Clayton Homes recently announced renovations to an existing factory that will allow it to produce 3,000 homes annually. But overall Clayton fits the basic pattern, as production of its 49,000 homes is spread amongst 41 production facilities.

Within the manufactured home facilities, we see the adoption of various efficiency-enhancing strategies compared to how work would be done on a conventional jobsite. As with Ford’s assembly line, work is arranged so that tasks take place at worker height, eliminating extraneous movements like bending or stretching. With conventional home construction, workers first complete the outside shell of the house to create a waterproof environment to work in, but this means the remaining work must be done within the cramped interior of the partially completed house. Manufactured homes, built under a factory roof, aren’t subject to this restriction and can be built from the inside out. Permanent stations can be set up with equipment for various repetitive operations, such as cabinet assembly. (We see this same sort of strategy adopted in large-block ship construction, with as much work as possible done outside the ship on prefabricated blocks, minimizing the amount of work that needs to be done in the cramped conditions of the assembled ship.)

However, the work remains a highly labor-intensive operation. Workers are in large part doing the same tasks that they would be in conventional construction; those tasks have just been made somewhat easier to perform. Equipment use is likewise somewhat modest: we don’t see the huge arrays of robot arms or automated machinery that we see in car manufacturing or other mass production industries. Per their annual reports, the value of the equipment that Nobility Homes, Legacy Housing, and Cavco operate is just one-third to half the value of the actual buildings. At a car manufacturer like Ford, by contrast, the value of the equipment and tooling is over three times as much as the value of the buildings that contain them.

Part of the reason manufactured homebuilders use a large number of low-capacity factories is high transportation costs. Both Nobility Homes and Cavco note in their annual reports that the cost-effective shipping range for their products is around 350 miles (around a day’s drive). This is a result of dollar density — the value of the product divided by the volume or mass of it. Products with high dollar density, like electronics, are very valuable in proportion to the amount of space they take up and can be effectively shipped long distances; iPhones can be made in a factory in China and then shipped all over the world. Products with low dollar density, like toilet paper, have low prices in proportion to the amount of space they take up, and are harder to ship long distances. If it costs $2,000 to ship a container from China to the US, that $2,000 will be a small fraction of the value of the cargo if the container is filled with iPhones, but a large fraction of the value of the cargo if it’s full of lumber or kitty litter. The lower the dollar density of a product, the less cost-effective it is to ship it long distances. Manufactured homes have very low dollar density, and thus can’t be shipped very far cost effectively.

But transportation costs can only explain part of this distributed manufacturing strategy for manufactured homes. For one, if there were substantial economies of scale at work, it would be worth it for manufacturers to ship longer distances in spite of the higher costs; transportation costs are proportionately high for manufactured homes, but they’re not that high, on the order of a few dollars per mile. Transportation costs thus suggest a sort of ceiling as to the extent of economies of scale that can be achieved for manufactured homes. For another, manufactured home producers often have multiple facilities much closer together than the cost-effective driving distance. Legacy Housing has factories in Commerce, Texas, and Fort Worth, Texas, that are around 100 miles apart. Cavco has three factories in the Phoenix metro area, two factories in North Carolina that are 120 miles apart, and two factories in Georgia that are less than 75 miles apart. If there were substantial economies of scale at the factory level, we’d expect these nearby factories to be combined into larger operations.

Thus even in a homebuilding sector with many tailwinds enabling economies of scale, scaling effects still appear to be relatively minor. Manufactured housing is produced in a controlled factory environment and built to the standards of a single national code, both of which should enable the highly repetitive production necessary for capturing economies of scale. And yet the scale of most production facilities is low, factories employ little in the way of high-volume automated equipment, and very small-scale operators producing a few hundred homes a year appear roughly as competitive as companies producing tens of thousands of homes a year. These patterns suggest that there’s something about the homebuilding process itself that makes capturing economies of scale difficult.

What prevents economies of scale in homebuilding?

The easiest way to understand the difficulties of achieving economies of scale in homebuilding is to look at the relationship between input cost and output cost in various industries.

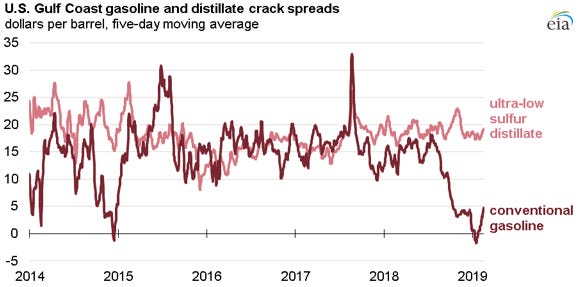

The graph below shows what’s known as the “crack spread” for gasoline production in the US Gulf Coast between 2014 and 2019. The crack spread is the difference between the price of crude oil and the wholesale price of gasoline. It essentially tells us how much margin oil refineries have to work with — how much they can afford to spend on the various production processes per barrel of oil processed. We can see that the crack spread for gasoline was typically around $15 a barrel for most of this period, compared to a crude oil price of around $50-70. In other words, the ratio of the price of wholesale gasoline to the price of crude oil was around 1.2 to 1.3.

An oil refinery is an enormous, expensive process facility that costs billions of dollars to construct. But because refineries produce such a large amount of gasoline and other petrochemicals, this cost can be spread very thinly across the refinery’s output, and the price of the final products is not all that much higher than the costs of the material inputs.

Likewise, consider car manufacturing. A few years ago, car industry analyst Munro & Associates conducted an analysis of the production costs of BMW’s i3 electric car. The report breaks down the various costs of production for different parts of the car, letting you see the cost of the inputs, the number and cost of the various operations performed on it, and the cost of the completed assembly.

We can see that the ratio of output costs to material input costs is higher than with gasoline production, around 1.8 on average. For complex manufactured goods that require a lot of distinct operations (the motor assembly alone has almost 5,000 parts and almost 30,000 assembly steps), it’s hard to achieve an output-to-input ratio as low as can be seen in a scaled continuous chemical production process.

More generally, any factory or production process will take some physical inputs, perform some set of transformations on them, and produce some series of outputs. If those transformations are involved or complex, requiring a lot of expensive machinery or labor-intensive operations, the ratio of the cost of the outputs to the cost of the inputs might be quite high. But even with a large number of complicated steps or very expensive equipment, this ratio can be driven down by taking advantage of economies of scale: spreading the fixed costs of your equipment out over a larger production volume, or using higher-capacity equipment or processes that has lower per-unit costs. As production volumes rise and a process gets more efficient, the ratio of the output costs to the input costs should theoretically approach one.

Elon Musk calls the ratio of the final cost of a product to the cost of its raw materials the “idiot index.” A high idiot index suggests a highly inefficient process with a lot of wasteful operations that could be dramatically improved. A low idiot index suggests a process with much less room for substantial improvements. (It was allegedly the high idiot index of rockets that convinced Musk he could beat existing aerospace companies and that SpaceX was worth pursuing.)4

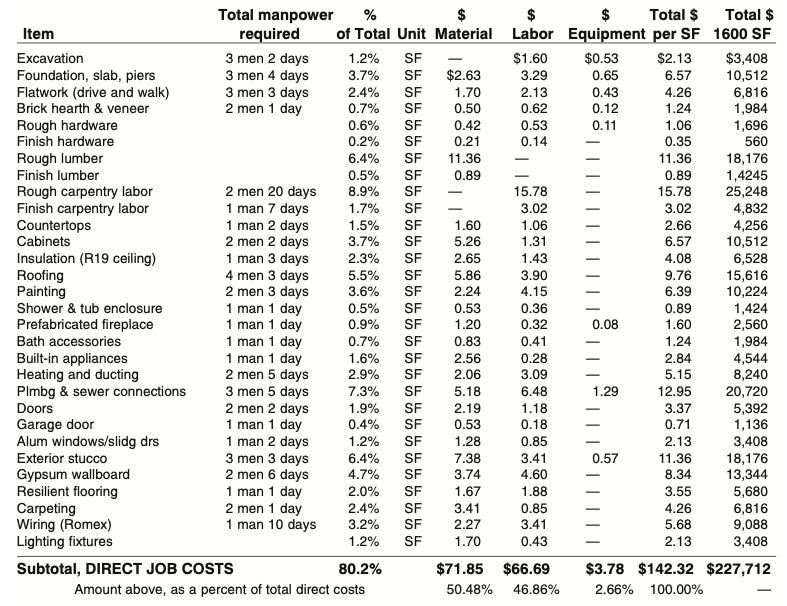

Armed with this concept, let’s look at the cost breakdown of a typical US single-family home, courtesy of Craftsman’s National Construction Estimator. The chart below shows the hard costs of construction: what it takes to put up the actual, physical building.

The most important takeaway here is that the hard costs of constructing a single-family home are roughly 50% labor and 50% materials. This means that the ratio of the costs of the output to the costs of the physical inputs (drywall, lumber, concrete, etc.) is around 2. This is a very low ratio: it’s only slightly higher than the ratio we saw with various BMW i3 subassemblies.

With car manufacturing, this low ratio is achieved by way of scale, spreading the costs of expensive equipment and hundreds of workers over a very large output. If BMW tried to assemble its i3 cars one at a time, outside of a factory, the output-to-input ratio and the overall costs would be vastly higher, the same way that the craft method of car building was far more expensive than Ford’s mass production methods.

In home construction, however, this low ratio is a product of the fact that the amount of transformation taking place on the inputs is relatively modest. It takes a relatively small amount of labor and equipment to transform lumber, drywall, concrete, shingles, and other building materials into a finished home.

The fact that the ratio between costs of constructing a home and the costs of the various materials is already so low is fundamentally what makes achieving substantial economies of scale difficult. For complex manufactured goods, when this ratio is high — when there are a lot of labor-intensive operations or transformations required to turn input materials into a final product — the strategy for efficiency improvement is relatively straightforward. Build some machine to perform some particular task, sequence it together with other machines performing different tasks, and then use those machines to produce as much output as possible. The machines might be expensive to develop and build, and you’ll need new, expensive workers to keep the automated systems running. But with high production volumes this trade-off is worth it: all these costs get spread out thinly, and the ratio of output costs to input costs trends downward. This is broadly what Ford did for production of the Model T, and it’s how production for things like lightbulbs evolved in the early 20th century.

But when the ratio between output costs and input costs starts out low, as it does with homebuilding, it’s hard to take advantage of this strategy: the potential savings are just too small. I’ve noted previously that it takes a lot of expensive automation to duplicate the efforts of a small number of construction workers with hand tools, and when I was at Katerra, executives would often bemoan how hard it was for their capital-intensive production to compete with “Bubba and his truck” — low overhead contractors using manual labor and not much else. The ratio of output costs to input costs doesn’t give enough “bite” for production economies of scale to act on, and there’s little to be gained in production economies by dramatically increasing the scale of your homebuilding operation.

Conclusion

Economies of scale are often one of the most powerful forces available for making some process more efficient. But economies of scale operate on the difference between the costs of the raw inputs to some process and the costs of the final product. When this difference is large, there are often substantial economies of scale that can be achieved. You can introduce automated equipment or other large fixed costs that reduce your overhead costs when spread over a large enough production volume. You can use larger-capacity equipment that has lower per-unit costs than smaller-capacity equipment. You can gradually make some process more efficient via learning-by-doing. All these strategies will whittle away the difference between your raw input costs and the costs of your final product.

But when this ratio is already low, economies of scale have little room to operate. Thanks to the relatively modest requirements for transforming construction materials into finished houses, homebuilding has the sort of ratio of output costs to input costs observed in high-volume production operations like car manufacturing. Once the low-hanging fruit is captured, such as more efficiently arranging the work in manufactured home factories, there’s little production efficiency to be gained from further increases in scale.

Thinking about economies of scale in terms of the ratio of output costs to material input costs does suggest strategies for achieving them:

You could find sectors of construction, such as nuclear power, where the ratio of output costs to input costs is very high, and thus have more opportunities for efficiency improvements.

You could vertically integrate backwards into the production of raw materials and components, in the hopes of driving down those costs.

You could find a way to use fewer and/or cheaper raw materials.

We’ll look at the viability of these strategies in future essays.

The combined starts of CBUSA members would make it the fifth largest single-family homebuilder in the US.

Newer versions of the Cost Estimator have no such deductions.

Clayton Homes also produces around 10,000 other types of homes each year.

Note that I’m using this concept slightly differently than Musk. Musk’s idiot index is about the costs of the raw materials, whereas for some of these examples I’m considering the cost of purchased components as well, but the basic idea is the same.

A low ratio does not necessarily mean that there is little room for efficiency gains. There could still be huge wins by making the *inputs* more efficient. Instead of seeing the cost of the battery in the BMW as "Well we can never get our input costs down lower than this", you could instead see it as "wow, if we can get this cost down then huge efficiency/profit gains are possible". Then you figure out why that battery is so expensive and optimize there.

It is the same for homebuilding. It is not that there are no opportunities for efficiency gains, it is that you are looking at problem only from the fixed level of the current large homebuilders. These companies outsource almost all the tasks that could be made more efficient - they are basically just project managers and financiers rather than home builders.

I think the more interesting question is: Why do current large US on site home builders all seem to fall into this model rather than following the typical producer model of looking for efficiencies and capturing the value add in these processes? Why are there no vertical (actual) home building companies that are training their own crews, buying up their suppliers, and developing new technologies to replace their costly inputs? It is a big enough industry to support this model, so there must be reasons why it does not happen.

Hong Kong tends to build residential high rises in identical batches. I'm curious if they successfully get any cost savings off that